The latest jobs report just dropped.

This is the most timely and accurate indicator of the state of the economy. Of course — like any data — it’s imperfect, but here’s today’s big story:

The U.S. economy is not sinking, but it’s also not surging. It’s treading water.

Is this the new break-even point?

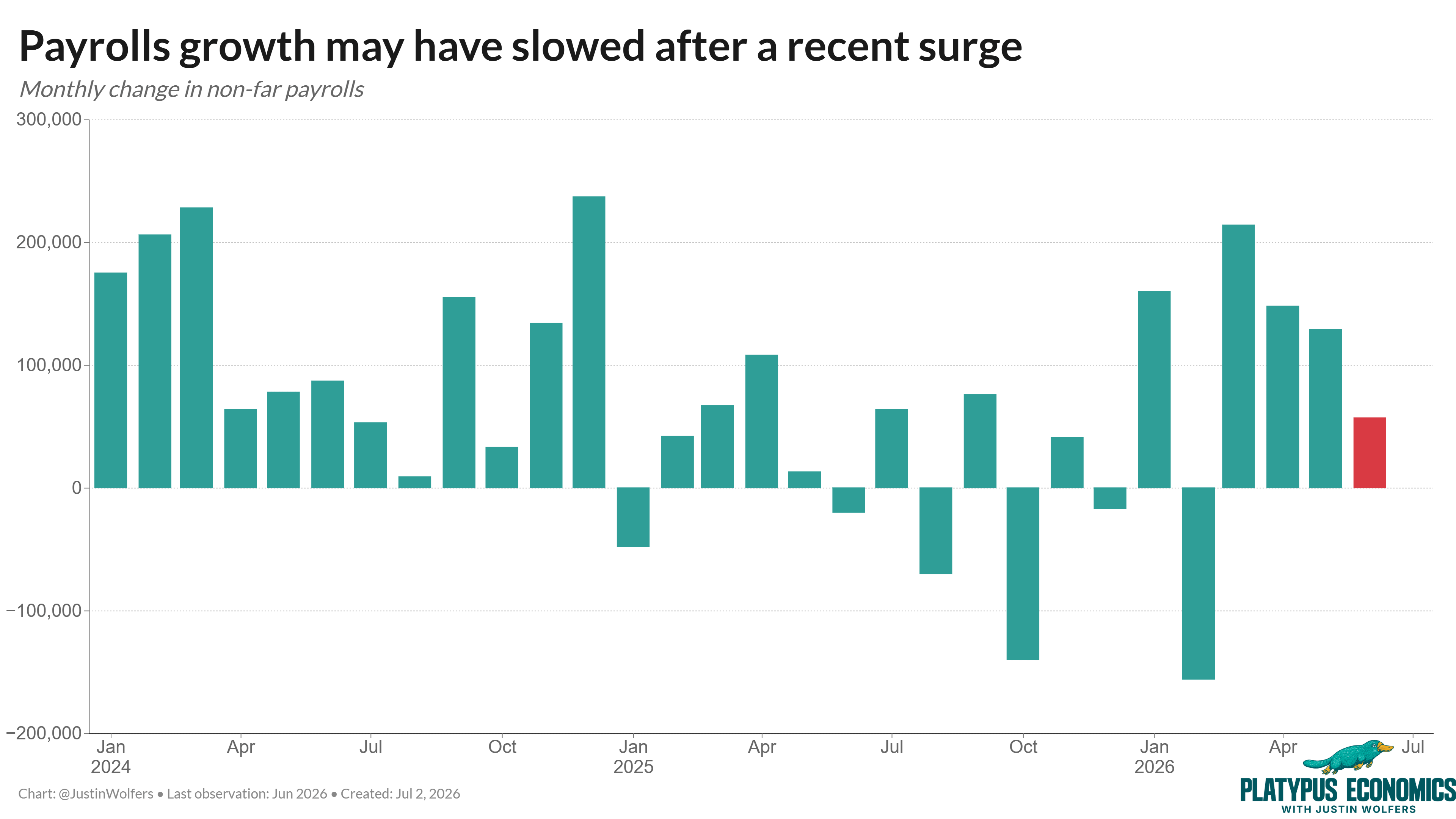

According to this report, employment grew by 57,000 in June. Markets were predicting a number closer to 120,000, so this comes in below expectations.

If I told you this number a few years ago, you would have (rightly) been unimpressed. But 2026 is a very different economy. And that has everything to do with population growth.

Under the second Trump administration, we’ve seen a sharp contraction in population growth. This is mostly due to immigration crackdowns. Fewer Americans means both less demand for stuff, and fewer workers looking to make that stuff.

Which means our break-even jobs growth number — the number of jobs we need to create each month, on average, to keep the economy steady — has also plummeted.

A few years ago, the economy needed to create around 150,000 or perhaps even 200,000 jobs each month just to keep pace with our growing population. We don’t know exactly what our break-even number is today, but it’s certainly a lot lower. If you want a ballpark estimate, it’s somewhere around 60,000 jobs per month (and I reckon a reasonable confidence interval probably allows for the possibility that it’s 50,000 higher or lower than that).

Below expectations, but not all bad news

Today’s report is particularly striking because it comes after a May report that was surprisingly strong — with both strong numbers for May itself, and positive revisions for the prior two months.

Now we can see that some of that growth was illusory.

The May jobs number was revised down by 43,000 (to a growth of +129,000), and April was revised down by 31,000 (to a growth of +148,000). Put these numbers together, and the three-month average — which is my favorite indicator of the underlying pace of jobs growth — is running at a little over 100,000 jobs per month.

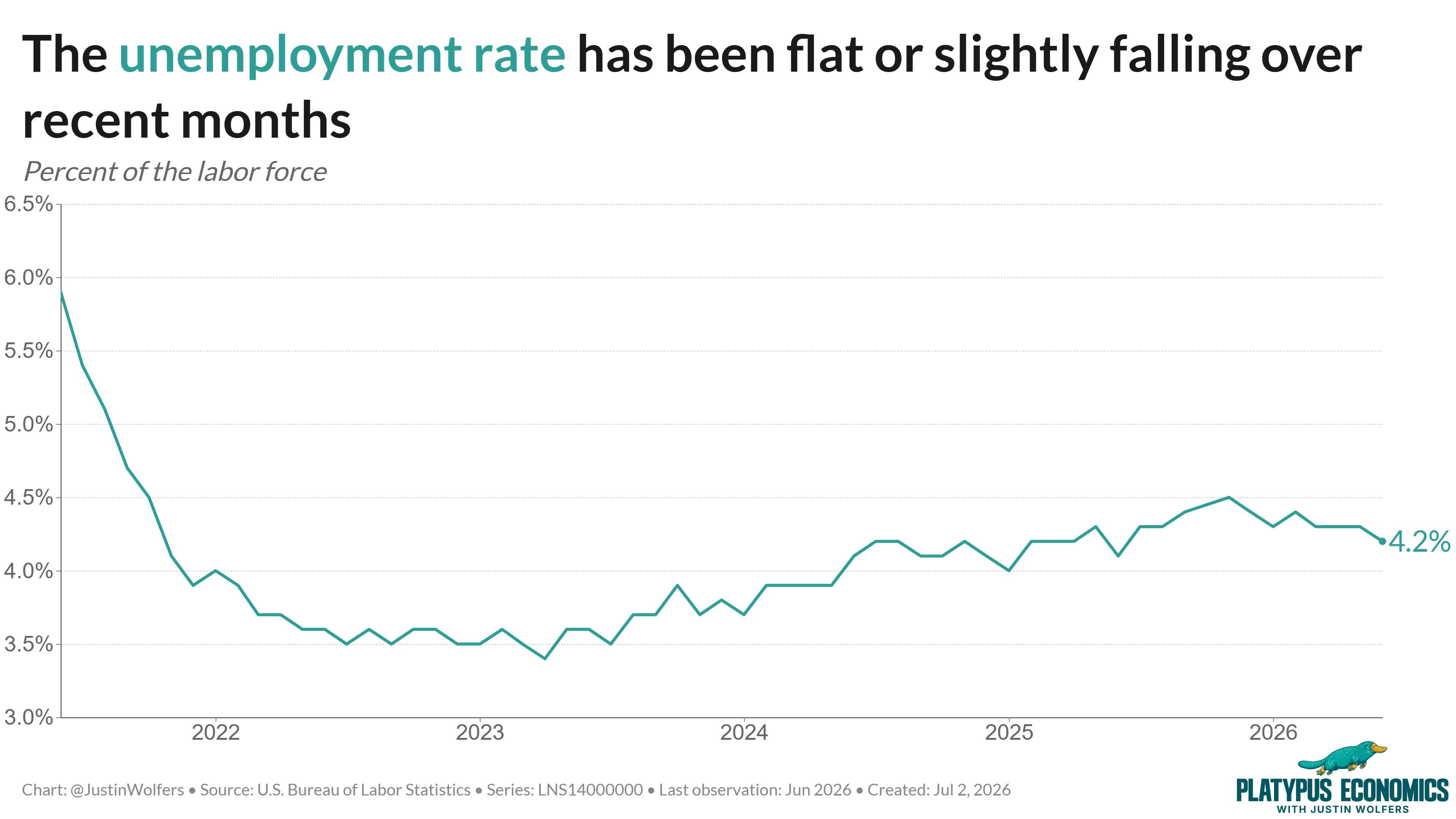

That’s probably enough to meet break-even job growth — and maybe even exceed it. Which explains why the unemployment rate has flatlined and may even be slowly drifting down.

What does this mean for the Fed?

This is another big question that comes with any jobs report. A month ago, two things were happening at the same time:

Inflation was surging (mostly because of the Iran war, seasoned with a side of tariffs).

The job market was surging.

When the job market surges, the Fed worries about overheating, and even more inflation. Which means last month they had two reasons to consider raising rates, and zero reasons for cutting them anytime soon.

This report suggests a more sustainable rate of job growth, and lowers concern about overheating. Nevertheless, inflation remains uncomfortably high. So the case for a rate rise has gone from unmistakably obvious to still reasonably strong.

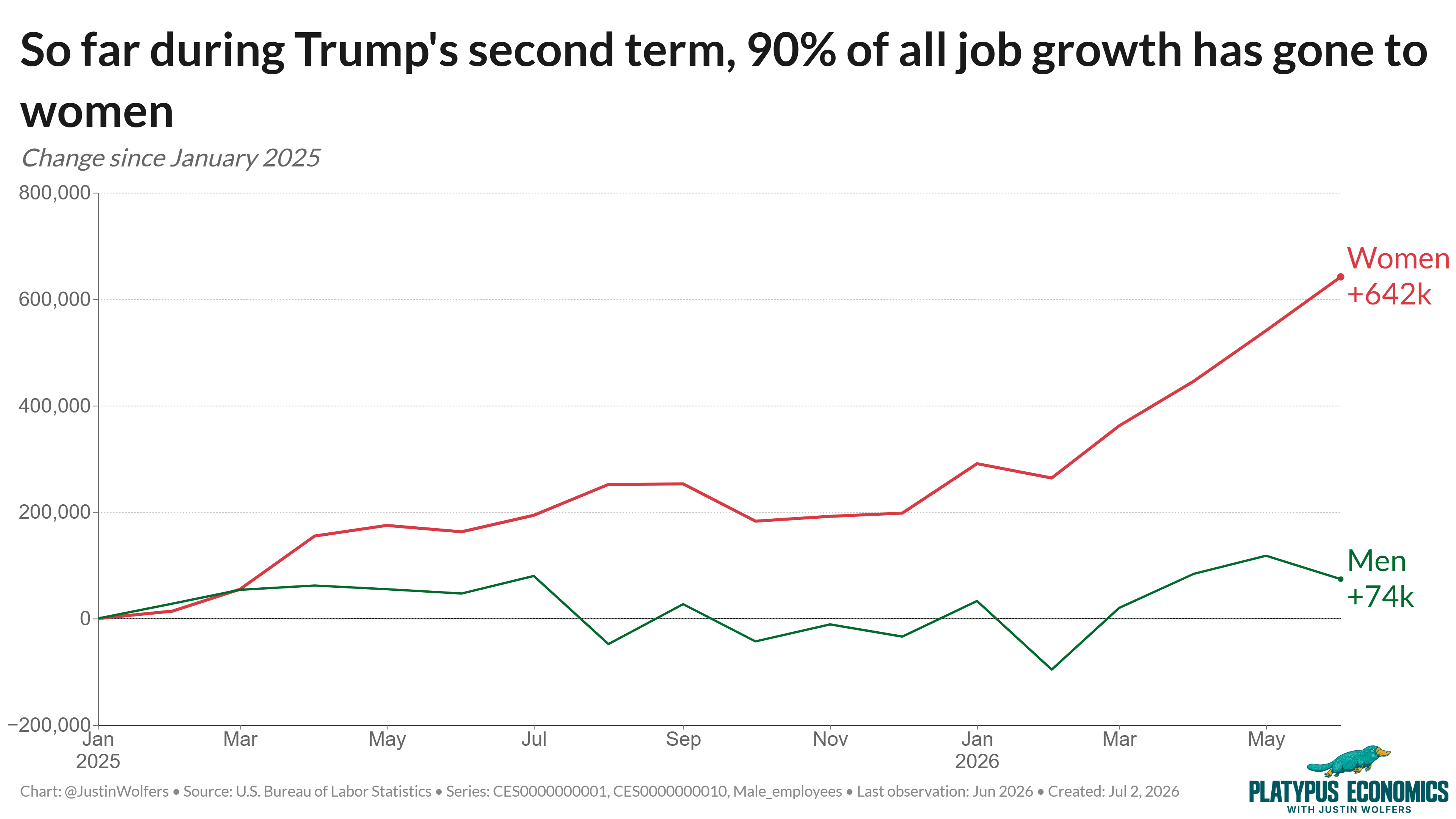

Women and healthcare continue to lead

It’s too easy for people to focus on this month’s number in isolation. But every month’s number is noisy, and every month gets revised. (And yes, I still believe these numbers are honest.)

It’s worth stepping back to think about how this current economic expansion is working as a whole. To that end, there’s a few longer-run stories we’ve been focusing on here at Platypus Economics.

The first is perhaps the most surprising.

Since January 2025 (the start of the second Trump administration), 90% of all new non-farm payroll jobs have gone to women. Women now hold a majority of all non-farm payrolls jobs (and have done so for a few months).

This is an interesting — and frankly, stunning — fact on its own. But it’s doubly interesting when you juxtapose it with the economic story this administration has been trying to sell.

Theirs is a story of hard hats and steel-toed boots and big boofy blokes getting back to the factory. But that’s not what’s actually happening.

Instead, this is an economy that has grown largely through the service sector in predominantly female fields. It’s a pink collar expansion.

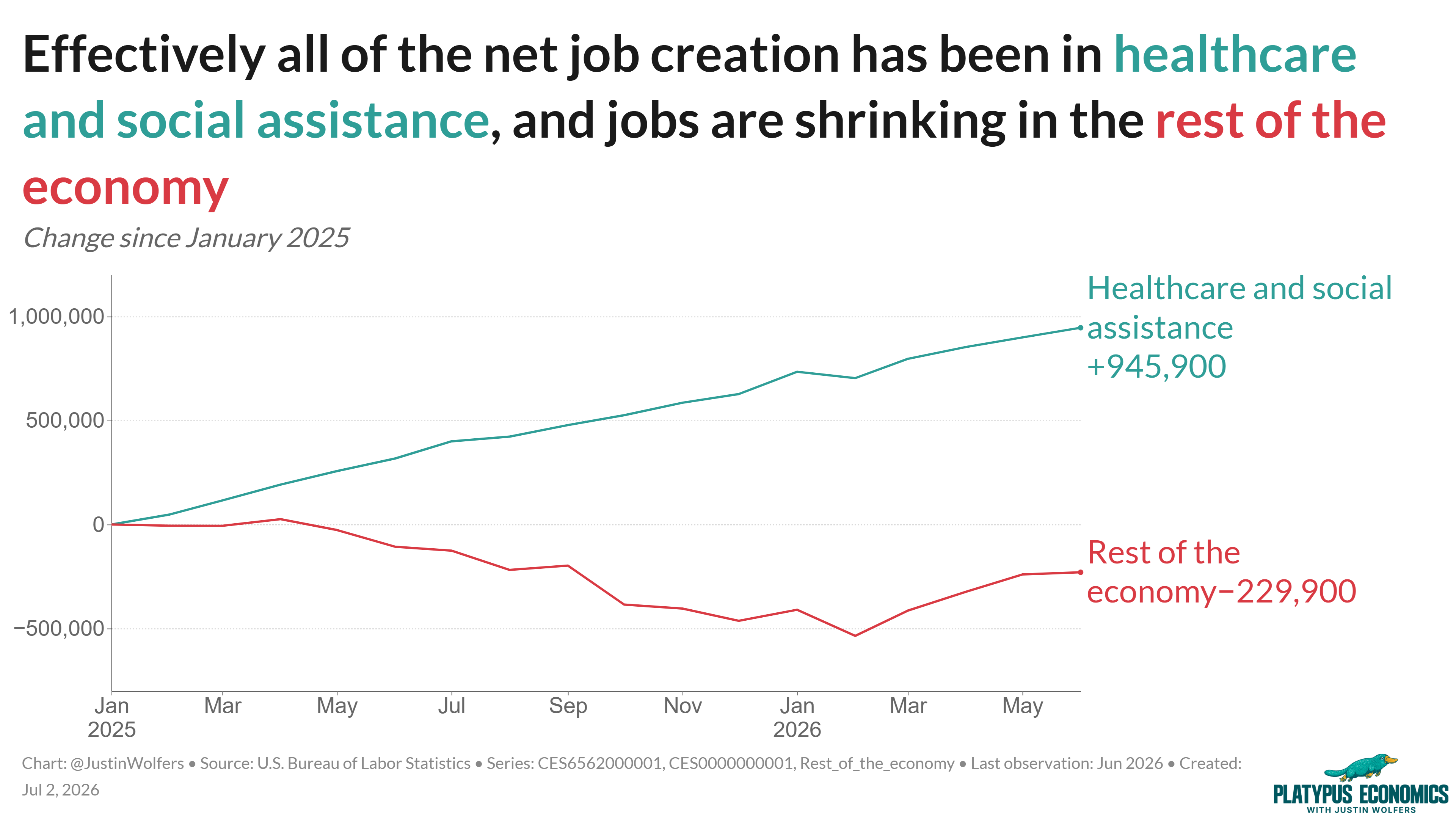

Which leads to the second trend we’ve been keeping our eye on: Since the start of the second Trump administration, more than 100% of job growth has come from the healthcare and social assistance sector.

If you take those jobs out of the picture, the rest of the economy has shed jobs overall.

Now, I wanted to be careful here. We don’t know that if the growth in healthcare hadn’t happened, the economy would have shrunk. A lot of workers would have likely moved across to other sectors and found other jobs.

But, as it stands, this is a strikingly unbalanced economy.

And that, in turn, helps explain why many people feel like economic opportunity might be shrinking. If you’re not in the healthcare sector — it is.

I expect this pattern of growth — of ongoing strength in the service economy at the expense of goods — to continue for decades. And it suggests that men may have to come to terms with the fact that the future of the economy looks very different from the past.

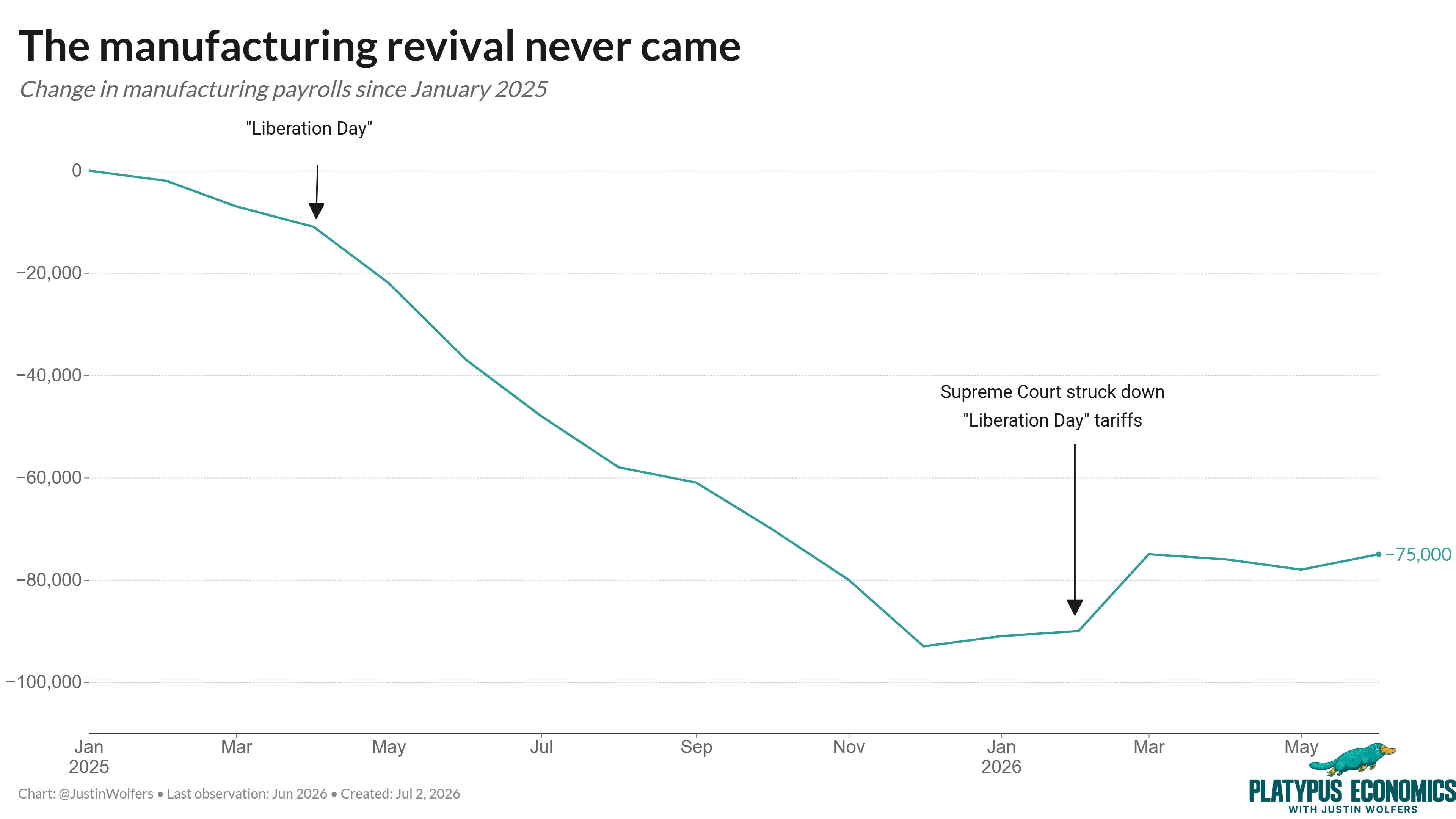

The manufacturing revival has not arrived

This brings us to the sector the administration’s been focused on most squarely: manufacturing.

Despite this focus, they’ve delivered literally nothing: The U.S. economy has been shedding manufacturing jobs for decades and has continued to do so over the last year and a half.

An ironic fact is that the first few months of Trump’s second term didn’t see too much of a drop in manufacturing employment.

But then came the “Liberation Day” tariffs.

The introduction of these tariffs — which were allegedly designed to help American manufacturing — is when the drop off really gained steam.

And when those tariffs were struck down by the Supreme Court? Well, that’s when we finally started to see a bit of a turnaround.

I honestly can’t say whether this is cause and effect, or merely a coincidence. But I know that the promised manufacturing revival has not arrived. And continuing to talk about it isn’t getting us anywhere.

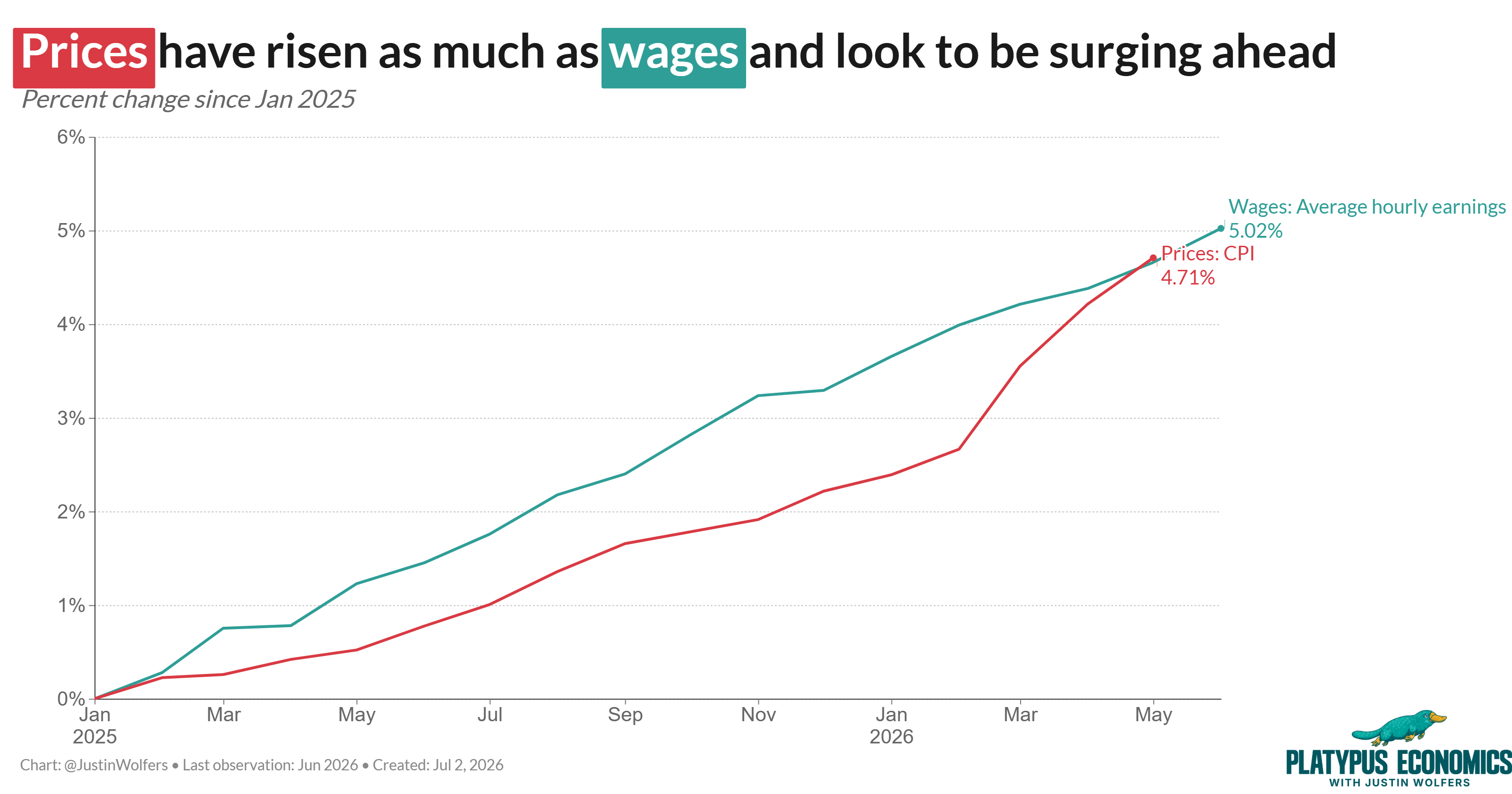

Are real wages falling again?

One final fact.

This jobs report also tells us about wage growth. But the most important story for many folks is what’s going on with wages relative to prices. This tells us how much your living standards are rising (or falling).

Today’s report gives us the wages part of that equation, and it reveals that nominal wage growth remains tepid. While we haven’t seen the price data yet, we have a pretty good guess that they’ll also have continued to rise, likely faster than wages.

Over the last 18 months, wages and prices had risen by exactly equal amounts. But my bet is that when we get the price data we’ll discover prices have gotten ahead.

This means that people’s real wages — on average — have fallen over the last 18 months. And they’ve been falling sharply over the past few. The sense that it’s hard to get ahead right now has some grounding in the data.

TL; DR

The economy’s not surging. It’s not sinking. We’re treading water.