War Rages On, Prices Keep Rising, And Wages Aren't Keeping Up

Don't panic — it's only food, fuel, and your rent.

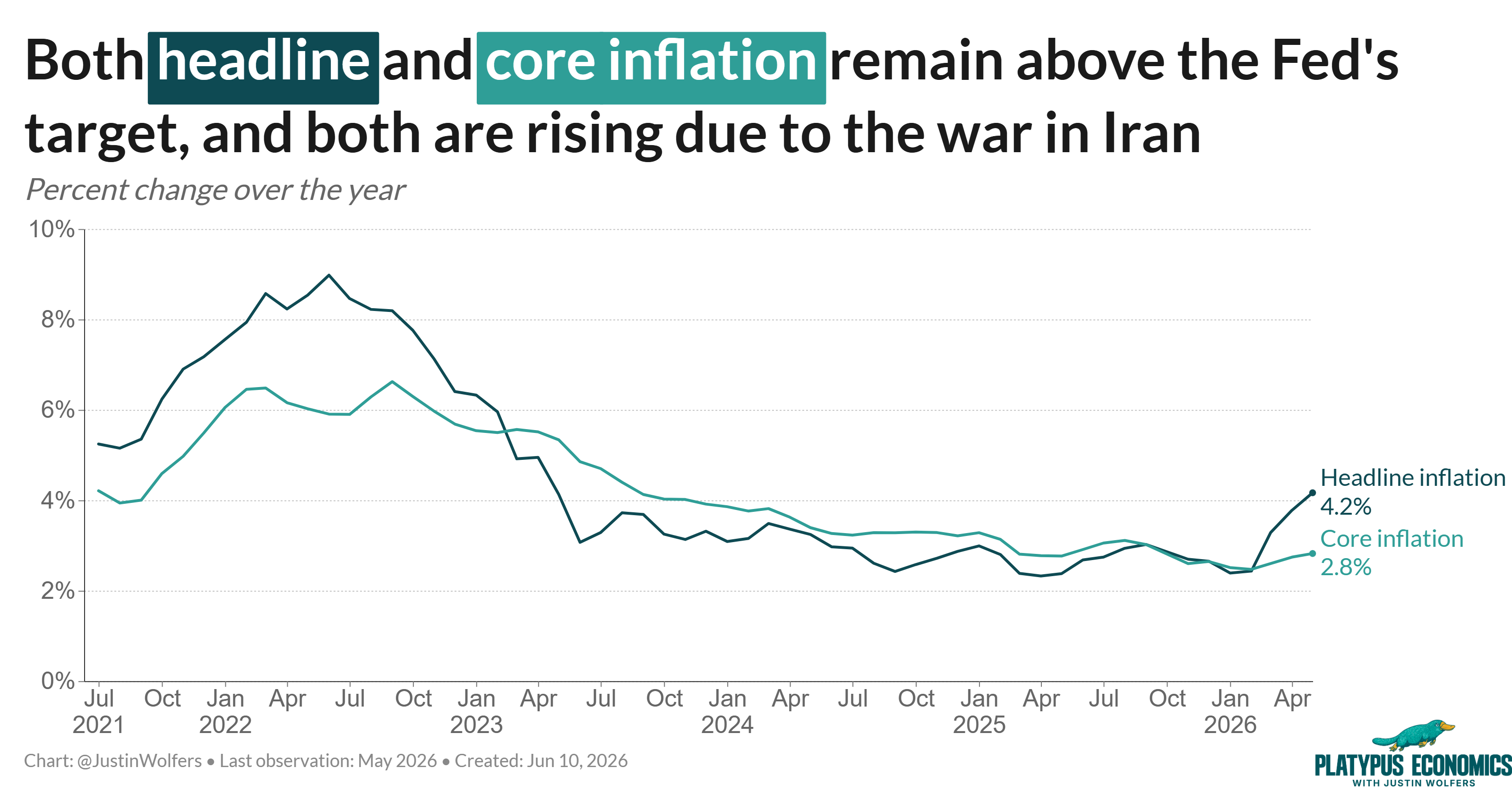

Today’s CPI report reads like a collaboration between two unhelpful supply shocks: a war pushing up energy prices, and tariffs pushing up everything else. Both headline and core inflation remain well above the Fed’s target of 2 percent, and neither is heading in the right direction.

Is inflation rising? Yes, but we have to be careful. The norm is to report on the rate prices rose over the past year, and the war has really pushed prices a long way above last year’s prices. Right now, the year-ended rate is rising, and it’s likely to keep rising for a while. So by this measure, inflation is rising.

But we also observe month-to-month price changes. In just the last month, prices rose by +0.5 percent (which is an annualized rate of nearly 6 percent). But that’s actually less than in April (+0.6%) or March (+0.9%). Basically this is what it looks like when an oil shock works its way through the economy.

From a purely mechanical standpoint, the year-ended inflation rate will keep rising as long as each new monthly inflation read is higher than the corresponding monthly reading a year ago. A year ago we were seeing monthly price rises of only about 0.2 or occasionally 0.3 percent. So you should expect to see even more dramatic headlines next month.

Headline inflation includes gas and food prices, which are particularly susceptible to disruptions in the Middle East. For now, core inflation, which strips these commodities out, remains more moderate at 2.8 percent, but it’s rising. The real question is how far the spill spreads. Oil doesn’t stay in your gas tank — it hitches a ride into your groceries, your Amazon order, even your haircut. That’s how an energy shock can quickly morph into a core-inflation problem.

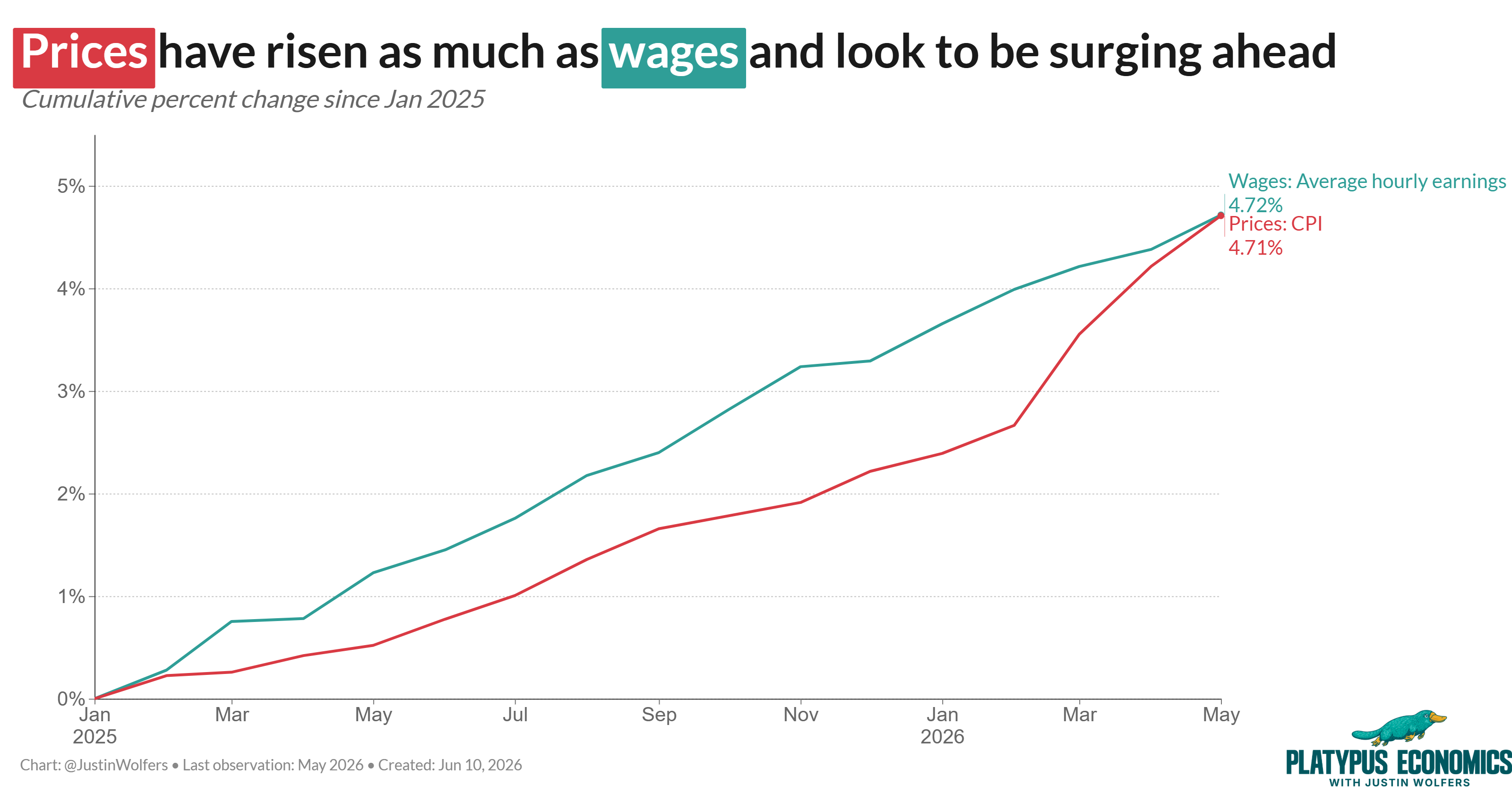

The sharp uptick in prices hasn’t been matched by a sharp uptick in wages. That’s usually the case — prices jump faster than wages. But it means that real wages — wages adjusted for inflation — are falling. This is not just due to the war with Iran: Real wages have been falling for the past six months.

As a result, real wages — that is, the purchasing power of the typical paycheck — haven’t risen a penny since President Trump returned to office in January 2025. Expect dozens of think pieces about wage stagnation. And the term “affordability crisis” will stick with us for a while.

I want to add a contrarian aside: Average wage data reflect the experience of the average American worker, but none of us is average. You’re not the average worker — you’re on a career path, a little more senior and a little better paid each year. And every year, well-paid near-retirees leave and fresh graduates start at the bottom. The mix churns even as you climb. So “flat average wages” and “most people got a raise” can both be true at once.

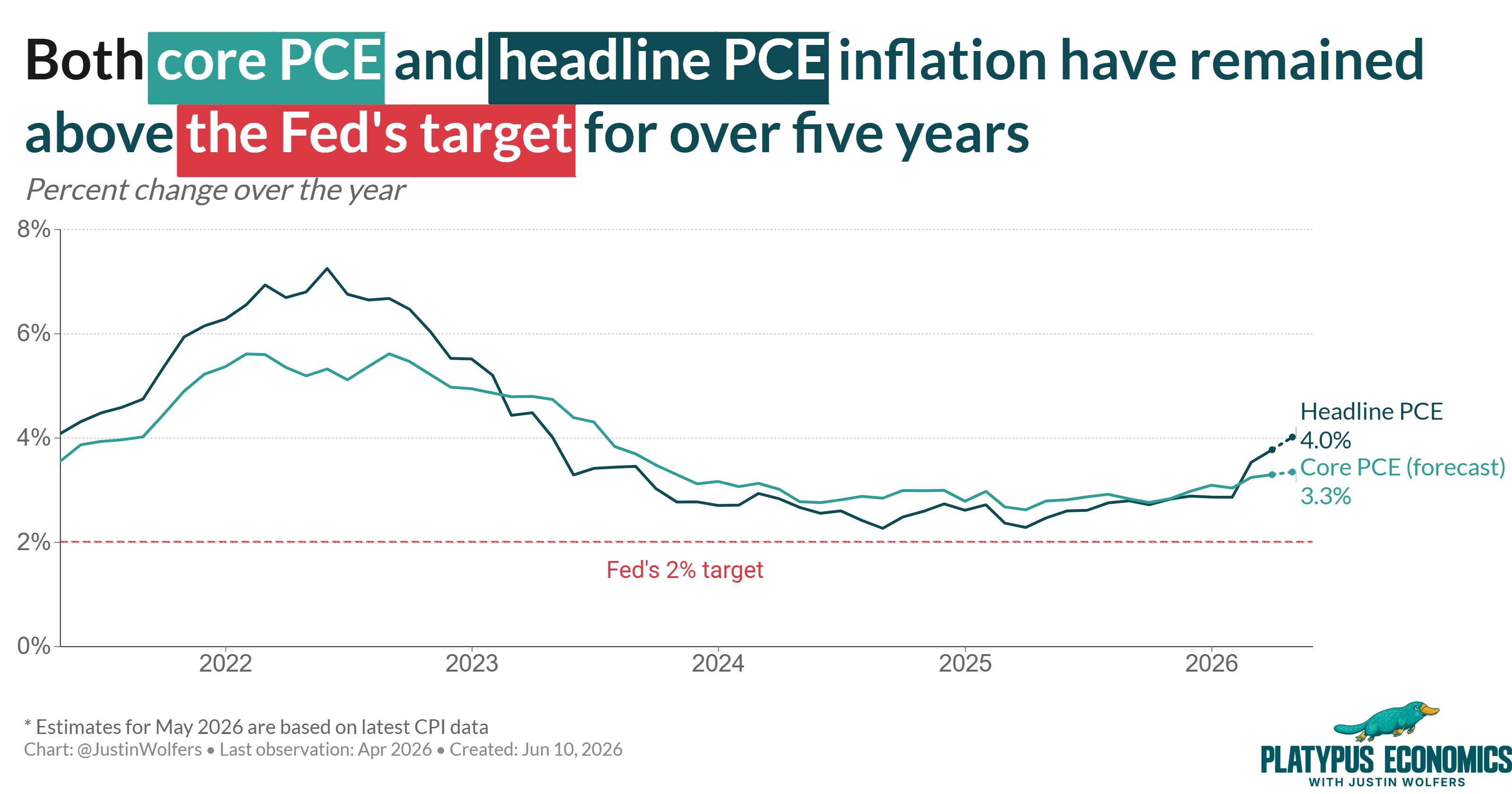

One more thought: The Fed tends to track a different inflation measure, called the PCE deflator. Today’s numbers come from a closely related measure, called the Consumer Price Index. With these data in hand, it’s pretty easy to form a good guess for what the Fed’s preferred measure will show when it’s released in two weeks’ time. So yes, expect another round of headlines describing higher inflation in the Fed’s preferred measure.

Kevin Warsh inherits the Fed mid-oil-shock — a rough hand for any inflation-targeter. Rougher still after five straight years above target. Good luck to him. Good luck to us all.

But, but but, I was told by Donald Trump that prices would come down on day 1! What happened? 🤯 Oh yeah, lies and incompetence. Maganomics sure does deliver one thing w/ consistency -- failure.

All kidding aside, will Kevin Warsh act as sane & stable leader of the fed or a partisan political actor? I hope for the former...

Brilliantly detailed.