On July 4th—our nation’s 250th birthday—the federal government trumpeted the official launch of Trump Accounts.

Here’s the pitch: Babies get a thousand bucks—a little stake in the stock market—and over time, that money grows into something much, much larger.

But here’s the reality: Trump accounts are actually two separate policies jammed into one. The first is a tiny, temporary giveaway for babies born in a very narrow window. The second is a brand-new, permanent tax break that will mostly benefit those who already have plenty of money to save. The first got all the headlines. The second is the more consequential policy.

Which means rather than giving poor kids a leg up, these accounts are far more likely to widen the gap.

They’re Selling the Baby Story

Let’s start with the bit the White House wants you to notice: some babies will get a thousand dollars from the government.

The administration has talked about the magic of compound interest, shown us glossy future balances, and wrapped the whole thing in the language of opportunity and ownership and getting a head start in life.

In other words, it’s extremely clever politics.

And here’s the thing: the idea of handing a child an asset at birth has a long—and frankly very progressive—history. But the progressive iterations (typically called Child Development Accounts or Baby Bonds) tend to be automatic, larger, and bigger for kids who start with less.

Take Senator Cory Booker’s proposal. It would have started with a public deposit at birth, and then piled on larger annual public contributions for kids from poorer families to offset unequal starting wealth.

Compare that with Trump Accounts: If a child is born between January 1, 2025 and December 31, 2028, they can get a one-time $1,000 government contribution—if a Trump Account is opened for them.

And that’s a very important, practical point you need to know: This deposit isn’t automatic. You’ve got to claim it. If your kid is born in the eligible birth window, you need to sign in through the IRS, submit Form 4547 (yes…really), and grind through the account election and activation process. (Which you should do: your baby will become a thousand dollars richer.)1

So yes, there’s a baby-bond-ish piece here. But it’s baby bonds after they’ve been through the wash a few too many times. They’ve faded, shrunk, and frayed. And come January 1, 2029 (conveniently just after the next presidential election) that bit vanishes altogether.

Which gives away the priorities, and brings us to the real policy.

The Real Policy Is a Tax Break

The lasting part of Trump Accounts isn’t the thousand-dollar seed money, but the tax breaks families get for pouring their own money into it. And this bit keeps on keeping on—long after the next election.

During childhood, families can chip in up to $5,000 a year (if they have it) to a Trump Account. And as part of this $5,000 cap, employers can deposit up to $2,500 in tax-free contributions.

These employer contributions are what economists consider a tax expenditure. Rather than the government writing you a check, they’re helping you out by collecting less tax. So the support flows through the tax code instead of through direct spending, but the overall effect—and the cost to other taxpayers—is the same.

And here’s another important bit: Since these employer contributions essentially operate as a cut in taxable income, this part is worth more for families in higher tax brackets. In other words, the government is making an even bigger contribution to the already-wealthy.

Now, when it comes to direct family contributions, the tax break is much weaker. When a family puts in its own money, there is no up-front tax deduction. And your kid will have to pay income tax once again after the money is withdrawn.

So the family-side benefit is mostly this: the money can grow without an annual tax on the gains (i.e. dividends, interest) while it sits inside the account. This is called a tax deferral. And while it can help, it’s often not the best deal. (More on that in a bit.)

This Mostly Helps Better-Off Families

Here’s the bottom line: the families struggling the most will hopefully grab the $1,000. But they’ll probably have to stop there.

Meanwhile, wealthier families are far more likely to add money year after year. They’ll also pick up employer contributions, and get more value out of the tax shelter since they’re paying federal income tax at rates that make them worth dodging.

Which means Trump Accounts aren’t so much opportunity-enhancing, as inequality-exacerbating.

Oh, and the $1,000 contribution only applies to babies born during the second Trump presidency. The tax-advantaged savings will be available forever (or until Congress repeals them).

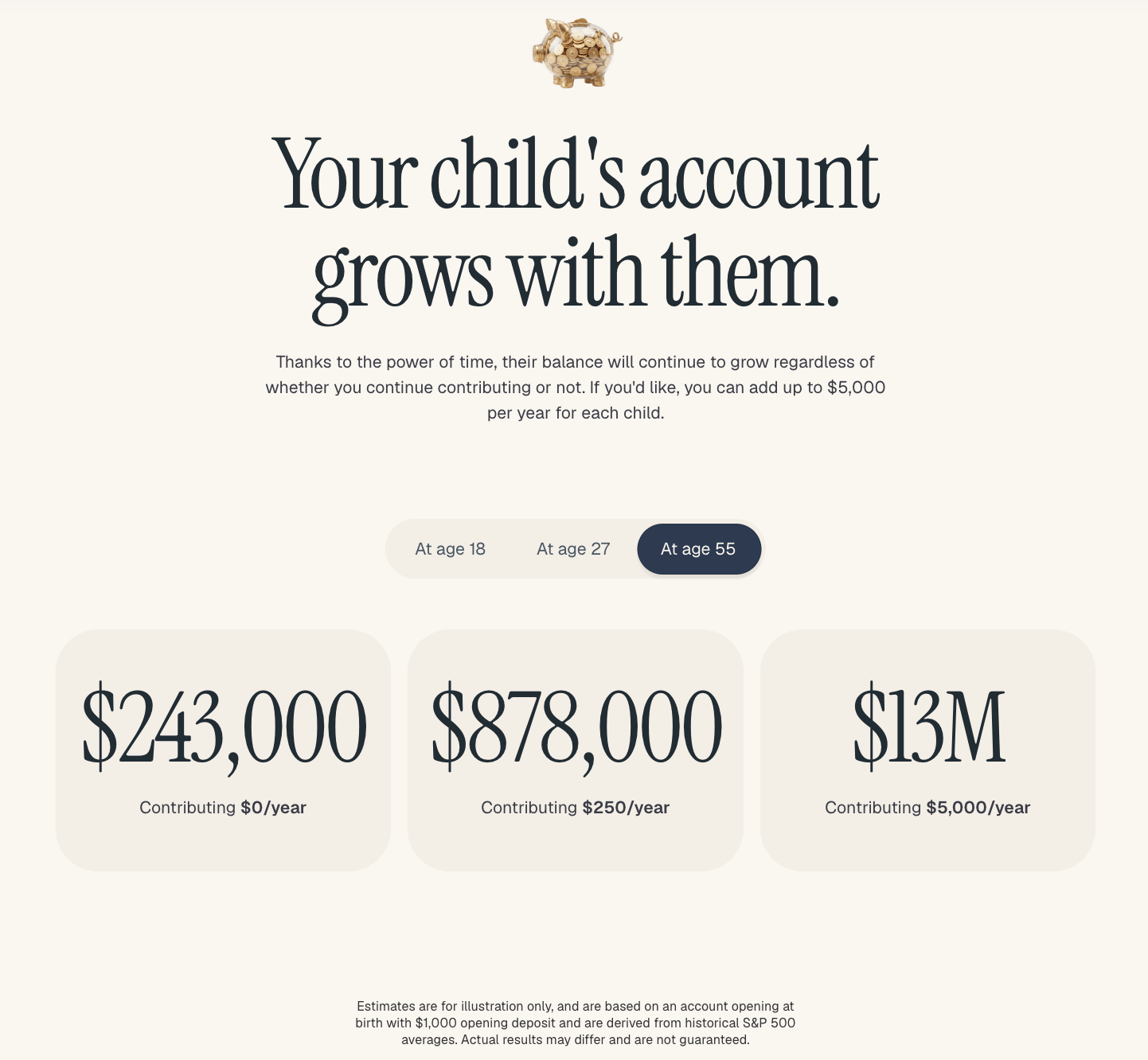

The Big Numbers Are Misleading

Now let’s dig into those big glossy numbers the administration has been peddling.

The White House put out projections at TrumpAccounts.gov showing that your kids could end up with enormous balances:

These numbers are ridiculous, dishonest and deeply misleading.

Now I’ll concede, the arithmetic is real—in the narrowest possible sense. The math maths. But it’s also GIGO — garbage in, garbage out.

These absurdly rosy projections reflect three assumptions that are wildly unrealistic for most families:

First: decades of private contributions. The big balances don’t come from the government’s one-time $1,000 contribution. They come from you, feeding $5,000 in every year for eighteen years. (Oh, and if you follow the footnotes, they also assume you feed another $7,000 per year into an IRA for the decade after that.)

Second: rosy market assumptions. They assume strong returns across long stretches. Quite literally, they’re assuming that the highest-ever recorded rates of return will conveniently repeat themselves when you invest in a Trump Account.

Third: inflation. A dollar in thirty years sounds like a dollar, but it really isn’t. Inflation-swollen future figures look impressive in a press release but turn out to be a lot less useful when you try to spend them in a grocery store. The honest way to go about this would be to present the numbers adjusted for the cost-of-living.

At the end of the day, these projections show a best-case, wishful-thinking scenario: families keep contributing, markets repeat record returns, and inflation apparently doesn’t matter.

Is This Even the Right Account for You?

But suppose you do have money you’d like to save for your kid. Is a Trump Account the best place to keep it?

For a lot of families, the answer is no.

Remember, on the family side, the main benefit is tax deferral—the money grows without an annual tax on the gains. That helps, but you’ve usually got better options.

For most families, Trump Accounts are less tax-advantaged than their alternatives, and would simply add another layer to an already cluttered savings system.

Let’s walk through those alternatives:

If the goal is education, a 529 is probably better—qualified education withdrawals come out tax-free (not deferred).

If the goal is retirement and your kid has earned income, a Roth IRA is usually the best option—the long-run tax treatment is typically more generous.

And if the goal is flexibility, a plain old taxable brokerage or custodial account can stack up surprisingly well—capital gains treatment often beats the ordinary-income treatment your kid will get on their Trump Account withdrawals.

If this all sounds like a lot of made-up words to you, my advice is even simpler: Do your homework. Talk with a financial advisor. Or with Claude or ChatGPT, who often give even better advice. (I’ve checked.)

Don’t put this off. It really matters. Ten minutes of reading could be worth thousands of dollars to your kid.

So where does this leave us?

I don’t want to overstate the criticism. If your kid is eligible for the $1,000, you should claim it. Free money is free money. (Well, it’s not free to the rest of us, but you get the point.)

And if some families use this as one more savings tool—that’s fine, too.

But let’s not pretend this is some great equalizing reform.

The baby-bond bit is small, temporary, and gone in 2029. The lasting bit is another tax-favored account—one whose benefits mainly flow to high earners with employers willing to contribute.

If you actually wanted to attack inequality, you’d make the public contribution bigger, permanent, and better targeted to those who need it. If instead, you wanted to hand already-comfortable families one more tax-advantaged shelf to store their money, you’d build something that looks a lot like this.

And here’s the most important lesson: Not every policy with a smiling baby on the label is about equal opportunity.

Sometimes it’s just a temporary populist giveaway stitched onto a permanent tax break for those who need it the least.

I can’t say for certain this was designed to reduce uptake. But if you were designing something to reduce uptake…this is exactly what you’d do.