You may have noticed, I’m launching something new today: Platypus Economics.

I’ve spent decades teaching at the university level and I’ve loved every moment of it. But I also understand that most people never get access the ideas we discuss there — and they pay the price for it every day.

With Platypus Economics, I want to open the tent and spread the wealth. Because the gap between a good decision and a bad one can change the course of your life. Because economic literacy isn’t a luxury — it’s a necessity. And because everyone, not just the privileged few, deserves the tools to see the world clearly.

To kick things off, I’ve decided to start with a topic that perfectly illustrates why understanding economics is crucial to good public policy — and why debates about it often go so wrong.

That topic — the federal deficit. Thrilling stuff, I know. But stick with me. You see, a lot of economics can seem counterintuitive at first glance. A bit backwards and confusing. Honestly, a bit like . . . the platypus.

When the British first saw a platypus, they actually thought it was a hoax. An egg-laying mammal with a duck bill and venom? Sure, mate. But the platypus wasn’t make-believe, it just didn’t follow their preconceived “rules” or categories.

The same thing happens in economic debates all the time. For example, people hear the word deficit and think the answer is obvious — deficits are bad. End of story.

But that’s too simple. Sometimes deficits are smart. Sometimes they’re dangerous. The important question is not whether a deficit exists. But why it exists, whether we can afford it, and whether it makes sense for the world we’re living in right now.

The basics — and a note about scale

Let’s start with the basics.

Our deficit is the gap between what the federal government spends in a year and what it collects in revenue – mostly through taxes. Our debt is the accumulation of all the past deficits we haven’t yet paid off.

Pundits often treat the deficit as if it were a household overspending at the shops. As if the answer is simply: spend less, balance the books, job done. But a government is not a household. It taxes. It borrows in financial markets. It manages recessions and wars. And it sits inside a growing economy.

What matters is not whether we have a deficit, but how that deficit compares to our capacity to pay.

You can think of a deficit a bit like a mortgage. A $500,000 mortgage could be crushing for one family, but fine for another. For this reason, deficits and debt are typically measured relative to a country’s income – or GDP.

Another thing economists consider is how fast that GDP is growing. If a country’s economy is growing faster than the interest rate on its debt, it’s easier to sustain that debt over time.

When deficits are the right policy

Sometimes, running a very large deficit — even compared to GDP — is exactly the move a responsible government should make.

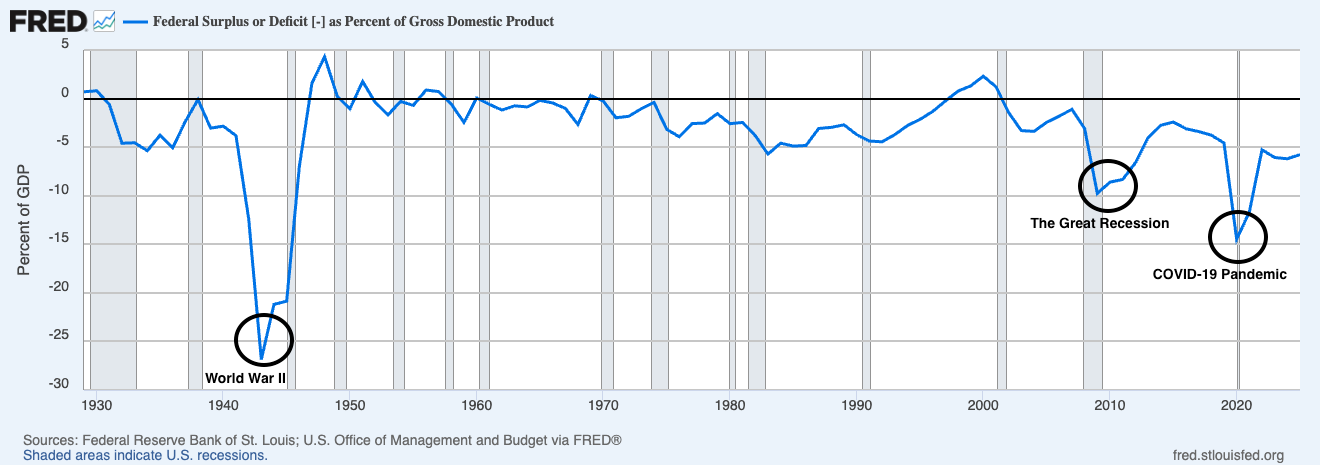

Think about World War II. The financial crisis of 2008–09. The pandemic in 2020. In each case, the government ran a remarkably large deficit because the country faced a genuine emergency — moments when the private sector couldn’t do the job on its own and leaving policy on autopilot would have meant failing to meet the moment.

During a war, resources must be mobilized fast. During a financial crisis, households pull back, firms stop investing, banks get wobbly, and demand collapses. During the pandemic, governments told citizens to stay home to stay healthy, and they shut down large chunks of the economy.

Now there are real debates to be had about how much spending is too much and how long it should last. But the basic principle is sound — deficits during a crisis can save jobs, stabilize incomes, and prevent a downturn from becoming a catastrophe.

Which brings us to a more interesting question — why is the United States running such a large deficit right now, despite the fact that we are not in a world war, a pandemic, or a major economic emergency?

Why today’s deficit is different

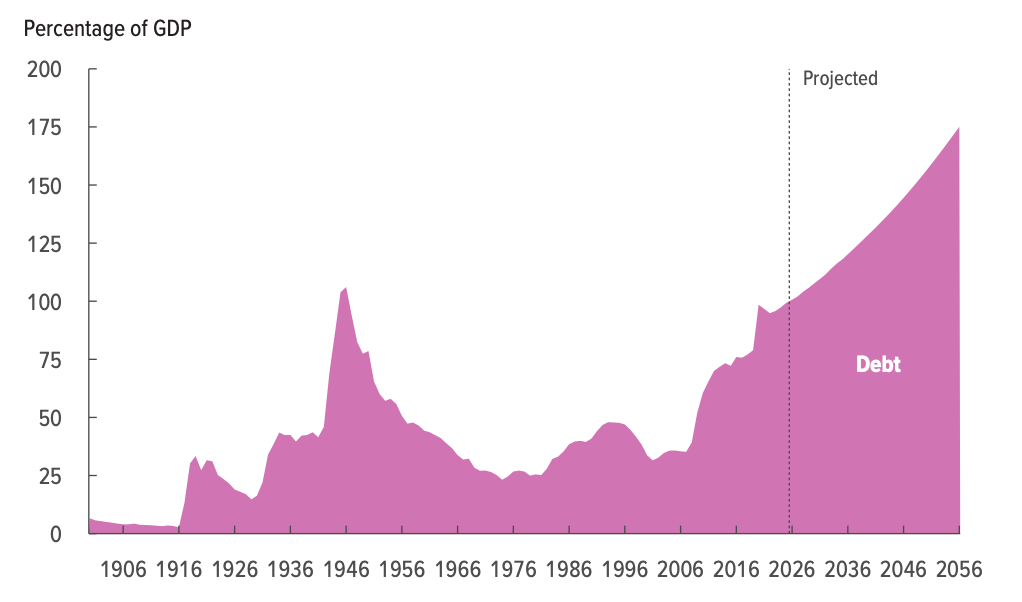

For FY 2025, the United States ran a deficit of $1.8 trillion — or roughly 5.8% of GDP. What’s more — the CBO expects this number to grow over the next ten years. According to their projections, total public debt will reach 120% of GDP by 2036.

This isn’t wartime mobilization. This isn’t the Great Recession. This is the result of a structural mismatch — a government that, year after year, is set up to spend significantly more than it collects.

An immediate consequence of this mismatch is that our interest payments will keep rising — occupying a greater chunk of our federal budget every year. Right now, we’re already spending roughly a trillion dollars annually just on interest — money that builds no bridges, funds no research, trains no teachers. Just the cost of servicing old borrowing.

How we got here

So, how did we get here? It wasn’t through one decision, but a lot of them — over many decades and across both parties.

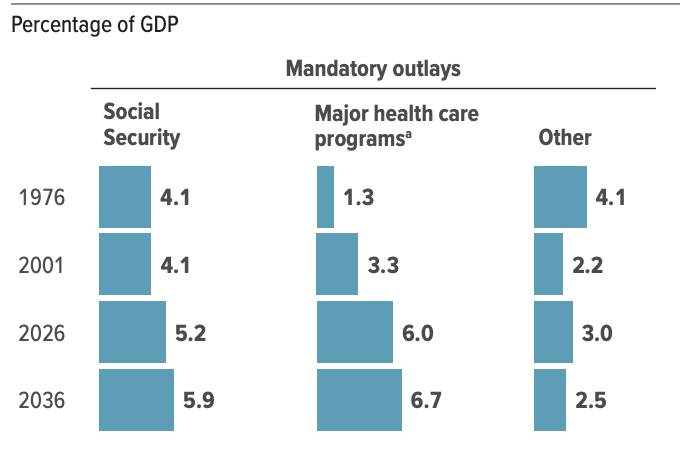

On the spending side: a large and growing share of the federal budget goes to Social Security, Medicare, and Medicaid. That’s mostly due to demographics and the rising cost of healthcare.

The population is aging. Baby Boomers are retiring. People are living longer. That’s a success story. But it also means promised spending rises over time.

Add in defense spending (approaching $1 trillion), and those ever-growing interest payments, and you have a budget with very little slack built in.

On the revenue side: over several decades, the U.S. has repeatedly cut taxes without matching reductions in spending. The Reagan-era cuts. The Bush-era cuts. The 2017 Tax Cuts and Jobs Act. And now, the One Big Beautiful Bill.

That last one is worth diving into, because the political framing around it has been particularly creative. The bill included several populist provisions aimed at working and middle-class Americans — no taxes on tips, no tax on overtime, deductions for seniors. Electorally potent policies.

But those cuts are temporary, set to expire at the end of 2028.

The cuts that primarily benefit the top 10% of Americans? They were extended permanently.

Reasonable people can debate the economic merits of a specific tax change. But this part isn’t ideology — it’s arithmetic: if you cut taxes without cutting spending by an equivalent amount, you increase the deficit.

Why you should care

I know what some of you are thinking. This is all very interesting, but I have a mortgage and a kid and a job and approximately zero time to worry about the national debt. Fair. So let me make this concrete.

Tradeoffs. Every extra dollar spent on interest is a dollar that can’t be spent elsewhere — infrastructure, scientific research, public health, schools, support for families, whatever your priorities happen to be. As interest costs rise, the room to do new things — or even keep doing old things — shrinks. This is happening now, not in some hypothetical future.

Fiscal space in a crisis. If another recession hits — or another pandemic, or some financial shock we can’t yet see — the U.S. will want the ability to borrow and respond forcefully. It still has that ability. But borrowing heavily in relatively good times means there’s less room to maneuver in bad ones. It’s like running up a credit card during a calm stretch of life: fine until it isn’t.

Long-run fiscal risk. I want to be careful here. The US is not on the brink of a Greek or Argentine fiscal crisis. We borrow in our own currency. Treasury bonds remain a foundational asset in global finance. The dollar continues to play a critical international role. These are all enormous advantages.

But these advantages are not an excuse for complacency. Trust can erode. Institutional credibility matters. And countries get into trouble not only by making one catastrophic mistake, but also by normalizing years of unserious budgeting. That’s what worries me.

The bottom line

Here’s what I’d like you to take away from all this.

Deficits are not automatically bad. Nor are they automatically fine. They’re a tool — and like any tool, we should be asking what problem is it the solution for.

During a genuine emergency, large deficits are not only smart, but necessary. Running a deficit of nearly 6% in peacetime, with no emergency on the horizon, is a different story. It reflects a structural choice — a government promising more than it’s raising, year after year — and it carries real costs that compound over time.

The public conversation about this often swings between two useless extremes. One side claims deficits never matter. The other says every deficit means national collapse. Both are wrong. The serious view requires context, proportion, and some basic arithmetic. That’s what I’m here for.

Welcome to Platypus Economics. Let’s make sense of this stuff together.