Something strange has happened in the American financial system that most people are completely unaware of — a huge chunk of borrowing and lending has quietly moved out of banks and bond markets and into private credit.

Private credit now accounts for roughly 30% of all loans made to riskier US companies. And it keeps growing.

So I wanted to know – is this a better, more innovative way of doing business? Or have we simply moved credit risk around, hiding it where the lights are dim and the supervision is lax?

I did some research, and I got an answer. It’s both.

The current financial system

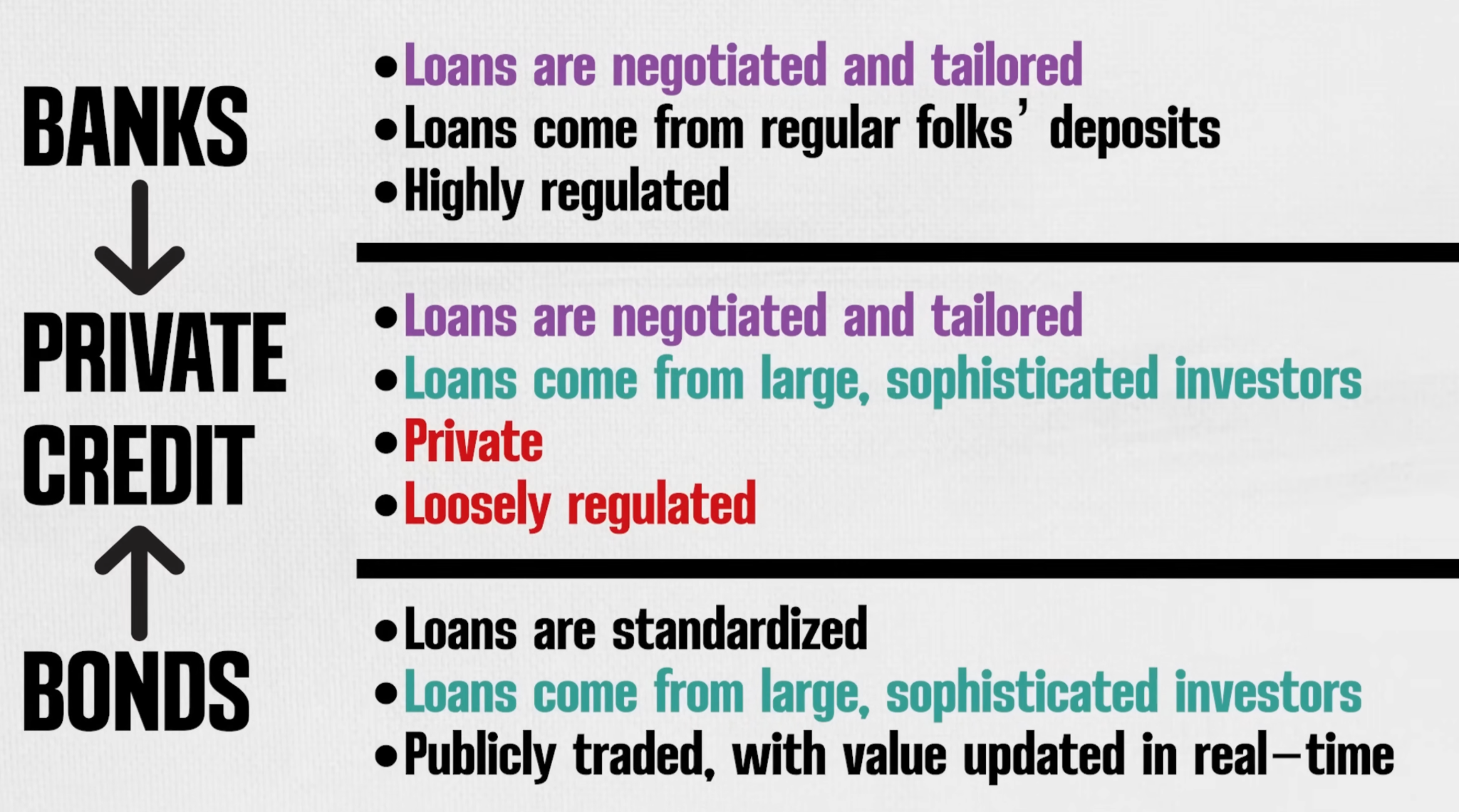

Right now, there are essentially three broad ways a company can borrow money: from a bank, via the bond market, or through private credit. All three are forms of “financial plumbing” — piping cash from lenders to borrowers. But they differ in important ways.

Let’s start with banks. Banks are essentially the visible plumbing in the front of a house. You can see the pipes, the pressure gauges, the shutoff valves. Banks take deposits and make loans based on what they know about you and your business, and they’re heavily regulated. That’s because a bank run can quickly rip through an entire economy.

Next, we have bonds. The bond market is like a large, municipal water system. It’s public and standardized. There’s plenty of eyes on it and prices update in real time. A bond is essentially an IOU – a piece of paper promising investors they’ll get paid back (plus interest) at some point in the future.

Now private credit.

With private credit, an investment fund lends directly to a business. The loan is negotiated and customized, built for and around the borrower. In that way, it’s similar to a bank loan, but the money comes from investors instead of ordinary bank deposits.

Crucially, private credit is much less supervised than banks. And unlike bonds, you can’t see its price change minute by minute as the loan gets traded on a public market. This makes its risks hidden from view, leaving open the possibility that small problems could spiral into catastrophe.

Continuing our metaphor, private credit essentially allows cash to be rerouted into financial pipes that run behind the walls. The water still flows, the house still works – in fact, it could work better than the old system, getting water where it needs to go faster. But since the pipe is behind the drywall, there’s a good chance you won’t spot a slow leak or notice the pressure building until the ceiling stains show up.

That’s the trade-off.

Who uses private credit?

Private credit typically serves what is called the “middle market.” These are midsized firms, who have an annual revenue somewhere between $10 million and a billion dollars. They’re not listed on the stock market and are often owned by private equity.

These mid-sized firms are usually too small to borrow easily in the bond market, but carry more debt than banks want to touch. They’re too private to want to open their books to the wider world, but too unusual to make the sort of off-the-shelf loan a bank likes to make. And sometimes, they’re valuable businesses – but without much physical stuff to borrow against.

For an economist, assets don’t need to be something you can trip over in a warehouse. But for bank managers, lending against invisible stuff can feel weird. This is why private credit is a big deal for technology and software companies. These companies often have customers, subscriptions, and code, but not a whole lot of physical items a bank manager can point to and feel good about calling collateral.

And that’s where private credit steps in. Private credit lending is usually run by “alternative asset managers.” These are not banks, but folks with a lot of cash who have the freedom to invest in things like buyout funds, real estate, infrastructure, and private loans. They’re firms with names like Blackstone, Apollo, KKR, or Blue Owl.

Where does their money come from? A variety of places including pension funds, insurance companies, university endowments, sovereign wealth funds, and rich folks who are looking to grow their money. So it’s not your checking account, but it could well be your retirement account.

How did we get to this point?

The recent growth of private credit can be traced back to 2008. After the global financial crisis, banks began to pull back on lending due to tighter rules, more scrutiny, and pressure from regulators not to make quite so many risky loans.

These regulations were understandable. But borrowers still needed money, and private equity stepped in to fill the gap. The water found a new pipe.

I should also mention the role of higher returns. The annual return on private credit over the last decade has averaged about 9%. Compare that with nearly 5% for high-yield bonds and leverage loans. If you’re a pension fund trying to pay retired teachers every month, that difference might be enough to keep everyone happy.

It’s tempting to tell this as a sinister story, but that’s too easy and not quite honest. Those borrowing and lending through private credit each have perfectly understandable reasons to like it.

For borrowers, they like that the money they need can come together faster. They’re confident it’ll actually show up. They’ve got fewer people to argue with. The loan can be shaped around their individual needs. And private credit lenders may still say yes, even when banks or bond markets get nervous.

Lenders like making these loans because they can charge higher interest rates. They can diversify, spreading their bets into parts of the economy the bond market doesn’t reach. And the results appear steadier than what you typically see in the bond market.

Now, some of that stability is real. If the borrower gets into trouble, these lenders are among the first to get paid back. But some of that smoothness is because these loans aren’t repriced in public every second the way bonds are. In public markets, bad news shows up immediately. In private credit, bad news travels slowly.

Why you — and regulators — should care

The Great Recession taught us that when the financial system creates trouble, we all suffer. Businesses struggle to make payroll. Some shut down. Others quit offering pay raises. Your job could be at risk and the whole economy can seize up.

In 2008, the problem was what economists called shadow banks. These were companies that were lending money as if they were banks. But since they weren’t actually banks, they weren’t regulated in the same way.

Remember, we regulate banks to prevent bank runs. And in 2008, we learned that shadow banks are in fact “banky enough” that they can still suffer bank runs — and those bank runs caused the entire global financial system to freeze.

So, are we set for a replay? Are we seeing that same set of risks rise again? Has the financial crisis receded enough from our collective consciousness that we’re about to repeat the same mistake? Is private credit simply a new form of shadow banking?

Well – partly yes, partly no. Yes, I’m a two-handed economist.

In the strict sense of the word – private credit is shadow banking. It’s lending that’s happening outside the formal banking system. And when risk moves into places where regulators can’t easily see, that should get your attention.

But the important question is not whether it lies outside the banking system, but whether a bank run is likely to happen.

A bank run occurs because of something called maturity mismatch – too many people demanding their money back today, while the bank’s money is tied up for months, years, even decades. You can solve the maturity mismatch problem through careful regulation and deposit insurance, or you can simply avoid it altogether.

Private credit typically tries to avoid it. They make long-term loans that come from investors who have explicitly agreed not to pull their money out straight away or even on any given day. Everyone goes in knowing their money is locked up for years, not days.

Unfortunately, this may be changing. Private credit has begun expanding beyond institutional lending towards letting regular folks get in on the action, without the same restrictions on pulling out their money. That should concern a regulator — or anyone whose seen It’s A Wonderful Life.

And bank runs aren’t the only thing to be concerned about. Another issue is that private credit is — well, private. That makes it harder to see where the risks are building and leaves more room for wishful thinking about what the loans are actually worth.

The thing is, at its current size, the private credit market has never lived through a long, grinding economic downturn. It’s never been stress tested at scale. All those pipes behind the drywall — we’ve never turned the pressure up.

So, should we be worried?

Here’s my best answer:

Private credit is useful financial plumbing. It solved real problems, but some of the pipes now run behind the metaphorical walls. And regulators should be looking more closely, especially in cases where private credit starts to promise a quicker exit to investors, or when it becomes more closely entangled with banks, insurers, and the existing financial system.

Let’s not be “panic in the stress” worried, but definitely “pay attention” worried. Because when Wall Street tells us the plumbing is working beautifully, the economist’s question is not “is the water running?” It’s “where are the pipes? Who’s inspecting them? And what happens when the pressure rises?”

And maybe — just maybe — “why is there a water stain on my ceiling?”