The Oil Market Isn’t Buying the White House Story

And neither should you

President Trump says gas and oil will “drop like a rock” once the Iran war ends. But futures markets disagree.

Futures markets are useful because they’re effectively a prediction market where traders bet millions of dollars on the future price of oil, and a bet is a tax on bullshit.

Right now, these markets are speaking clearly: oil will likely be expensive at least through the midterms.

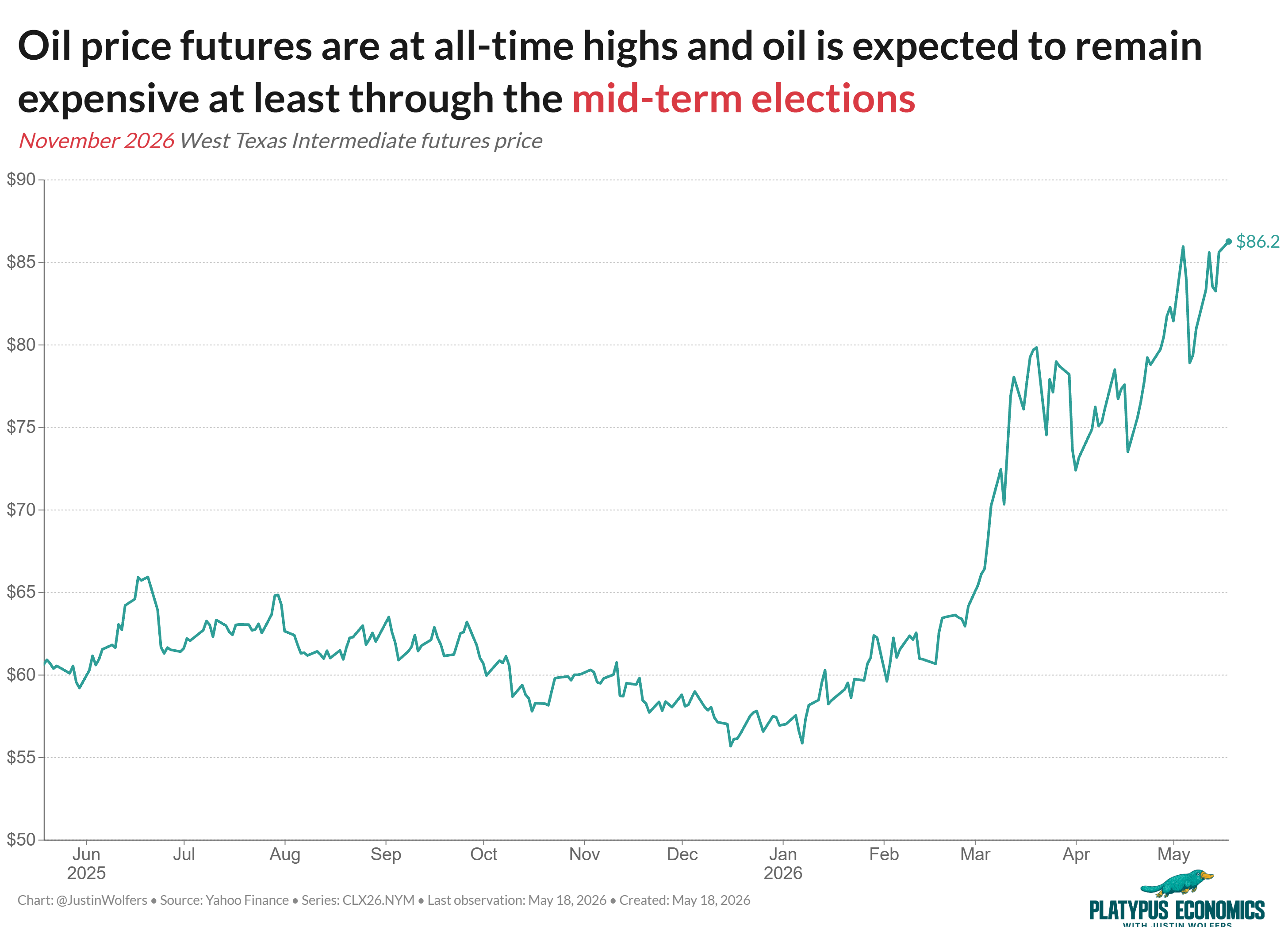

The November 2026 WTI futures contract — oil for delivery in the month voters go to the polls — is now at $86.20, an all-time high. That’s a 45 percent increase since the war began.

Since its increasingly clear that energy prices will still be a big deal during the midterm elections, I’m left to wonder: Why aren’t more Republican members of Congress panicking?

Even more concerning, this war-fueled rise in energy prices may still be with us by the next presidential election.

Like November 2026, the November 2028 oil futures contract has also moved up — from roughly $60 per barrel to about $71.

The longer-run effect is smaller, but it’s the same message: markets aren’t just pricing a bad week or a bad month. They’re pricing more expensive energy until at least the next general election.

The full set of longer-term consequences can be illustrated by focusing on the futures curve, which plots the price of oil for delivery at different dates.

Think of each point on the curve as the market’s price for oil delivered in a particular month. The near end tells you about the next few months. The far end tells you what traders expect years from now.

So let’s compare two futures curves: one from the eve of the war, and one from today.

Today’s curve slopes down, which tells us that markets expect oil prices to fall from today’s spike. Near-term oil is extremely expensive, while oil for later delivery is less expensive.

If I’m being generous, that’s the argument the White House is making.

But if you want to figure out whether the war is costly, that’s the wrong comparison. Instead, we should focus on the gap between the two lines.

Today, the entire futures curve sits above its pre-war levels. That means that — for every delivery date — markets expect oil to be more expensive than they did before the war.

The White House wants you to compare future prices with today’s spike. That comparison says relief is likely coming. Comparing the two futures curves answers a different — and arguably more interesting — question: how much has the war boosted oil prices, and for how long?

The answer: the Iran war is expected to reverberate through energy markets for years.

Futures markets can tell us what traders expect, but they can’t tell us exactly why. Maybe the market is pricing physical disruption — damaged export capacity, clogged shipping routes, depleted inventories, higher insurance costs, tolls and delays.

Maybe it’s pricing a broader risk premium — the world looks riskier, so traders are charging for the chance that something else goes wrong.

Either way, this is the part that should worry Republicans: the market isn’t pricing a disappearing problem. It’s pricing a lingering one.

I wish republican members of congress were listening to you and would start doing their job asking tough questions of the regime, and holding them accountable, but I'm guessing it won't happen. So, we all need to do what we can to make sure the house and the senate flip and leadership changes.

I suspect the Rs are counting on voter purges, gerrymandering, voter intimidation and legal challenges of fraud in the races they lose….