How I learned to stop relaxing and start worrying about the debt

Did I change, or did the debt?

I think this conversation with Derek Thompson is really worth watching (or listening to). Here’s why: Derek pushed me to do the best job I’ve ever done of really explaining the underlying economics of debt and deficits, and what we should and shouldn’t worry about.

If you watch or listen, you’ll also hear some personal discomfort, as we each spent years arguing against debt scolds.

Some personal backstory: I first met Derek during the 2008–09 financial crisis. He was a young econ journalist trying to make sense of an economy in freefall. I was a young economist trying to do the same thing, but with more equations, messier hair, and weaker writing skills.

I was wildly impressed by Derek; by any measure he was — and is — one of the best economics journalists of his generation. Since then I’ve watched him build Plain English into a wicked smaht podcast, move his writing to Substack, and write Abundance with Ezra Klein. (When I first heard early rumblings of that book, my honest reaction was jealousy — that Ezra had been smart enough to grab a superstar co-author before the rest of us could.)

Back to our conversation about debt and deficits: The funniest part is that each of us seemed to be trying to make the other one own the uncomfortable position of worrying about debt. Derek wanted to say: even center-left economics professor Justin Wolfers is worried about the debt. I kept trying to say: even center-left economics journalist Derek Thompson is worried about the debt.

That mutual reluctance is the story.

Back in 2009, we were each trying to impress on people a sense of urgency that if the government didn’t act decisively to put the economy back on track, it might leave scars that would last for years.

Sadly, we turned out to be right. The recovery from the Great Recession was remarkably slow. Remarkably painful. The Obama recovery plan was intended to be a first step: do something pretty large now, see how the economy responds, and go back to Congress if more was needed.

More was needed. But fiscal politics got weird. The Tea Party wave arrived. Partisan divisions hardened. And the deficit hawks — folks who warned that America simply couldn’t afford a bigger recovery effort — played a deeply unconstructive role.

Their argument was simple, and it sounded responsible: Debt is rising. Fiscal crisis is coming. We must tighten our belts.

But in that moment, it was mostly a bad argument, often offered in bad faith. Many of these so-called deficit hawks were less interested in fiscal responsibility than in preventing the government from doing more. The deficit became a respectable cloak for a much older instinct: they wanted smaller government, and if that sentenced a generation to joblessness, them’s the breaks.

The economics didn’t support their moral panic. Government debt was — by today’s standards — remarkably low. Interest rates were low. The urgent danger wasn’t that the United States would borrow too much to support recovery. The urgent danger was that it would borrow too little.

That formative experience made this week’s conversation feel so odd.

Nearly two decades later, both Derek and I find ourselves saying something that sounds uncomfortably close to what the debt scolds used to say. Each of us is concerned that our fiscal path might lead to a painful adjustment. (That’s a polite euphemism because I don’t want to sound too dramatic.)

So the question I kept asking myself was: Did I change, or did the economy change?

Did I get older and grumpier? Did I drift right without noticing? Did I catch whatever bug makes middle-aged economists start muttering about bond markets at dinner parties?

Here’s the first answer: the economy changed.

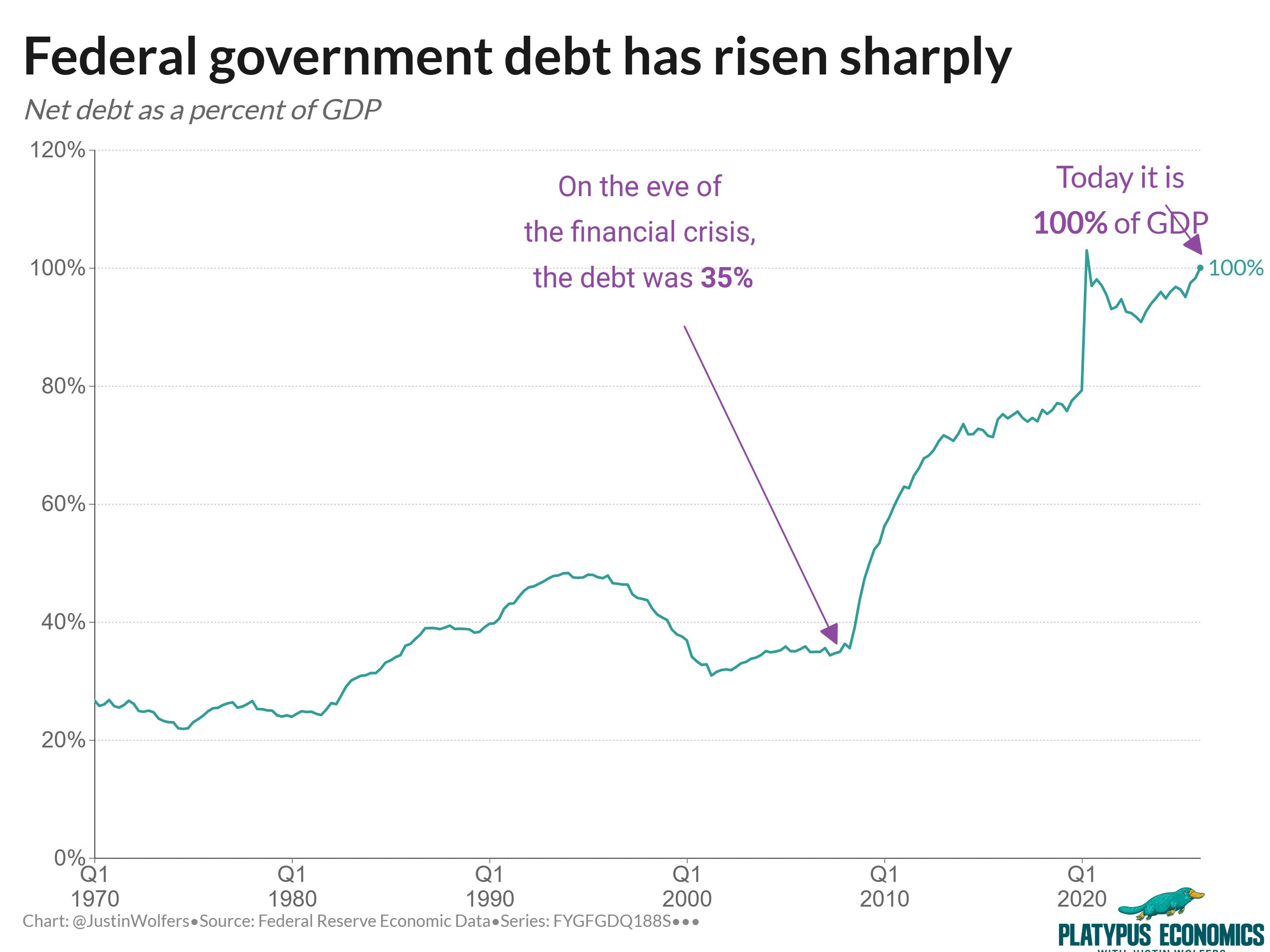

Federal debt as a share of GDP was around 35 percent on the eve of the financial crisis. It rose during that recession, never really came back down, and then jumped even higher again during COVID. It is now roughly 100 percent of GDP. So today’s national debt is nearly triple what is was when a younger Derek and a younger Justin weren’t so worried about it.

But debt is only half the picture. The other half is the deficit — how much we’re adding each year.

Today’s deficit would have looked extraordinary to pre-crisis America.

This is the part that would have blown young Derek’s and young Justin’s minds. If you had told us back then that the United States would be running a deficit of roughly 5.8 percent of GDP outside a world war, outside a financial collapse, outside a pandemic, we wouldn’t have believed you. And the idea that this would occur under a Republican House? Well, that’s crazy talk.

Today that enormous budget deficit barely gets a mention.

And so as the debt and deficit have changed, so have my concerns. When debt-to-GDP was much lower, I felt confident saying a fiscal crisis wasn’t coming. Now? As I said to Derek, “I am humble and I don’t have a clue.”

But that’s actually a thing: I have lost all confidence that I know a reckoning isn’t coming. Sorry for the double negative, but that’s how I got here. My conclusion — written in the positive voice — is that there’s a very real possibility that such a reckoning is just around the corner, a decade or two away, further off, or maybe it’s never coming. Derek is even more worried than I am.

I don’t want to oversell this. There’s no fiscal pumpkin that appears when the debt-to-GDP ratio hits 100 percent. What matters is the interaction between debt, interest rates, deficits, and trust.

Those are the big ideas. The video has the details.

Still, there are things that haven’t changed.

I still think austerity in a slump can be cruel, pointless, and self-defeating. I still think the deficit hawks of 2009 were wrong. I still think the government should act boldly in emergencies. If unemployment is surging and families are being knocked off course, the right question is not “how do we make the spreadsheet prettier by Tuesday?” It’s “how do we stop lasting damage?”

But a government that wants to act boldly in emergencies needs to build fiscal space in ordinary times.

That’s the uncomfortable middle-aged sentence. I don’t love typing it. I like it even less when Derek gets me to say it in front of a microphone.

We can’t do everything. We can’t have everything. Magical thinking is the disease, not the cure. And we can’t dismiss the arithmetic just because some of the people who used to talk about the arithmetic were using it as a dodge.

That’s why I’m proud of this conversation. I think it’s a genuinely useful place to start our fiscal debates — not because Derek and I solve the problem, but because we begin in the right place.

The deficit hawks were wrong then.

The debt is worrying now.

Those two sentences are not in tension. They’re the same framework applied to a different world. If you want to understand that world, start there.

Step 1. Stop deporting workers that would prefer to stay here and pay taxes. Step 2. Welcome a million more immigrants this year and every year there after that would love to come here and pay taxes. The Trump administration is solving the wrong problem.

We don’t pay taxes at the rates of the French, etc: No, we pay for every service the French, et al receive as government services. Child care, elder care, medical care, un- employment, education, etc. Tally up all these costs, include payroll taxes, WE PAY MORE, with every cost category marked up by a profit margin. This simplistic comparison is inadequate. US tax structure implies we’re all millionaires who can independently afford to hire servants, caretakers, tutors while living off the interest of our investments. No public services required!